Comparing Pension Plans vs Defined Contribution Plans

Analyze the differences between traditional pension plans and modern defined contribution plans for retirement.

Analyze the differences between traditional pension plans and modern defined contribution plans for retirement.

Comparing Pension Plans vs Defined Contribution Plans

Understanding Traditional Pension Plans: Defined Benefit Schemes

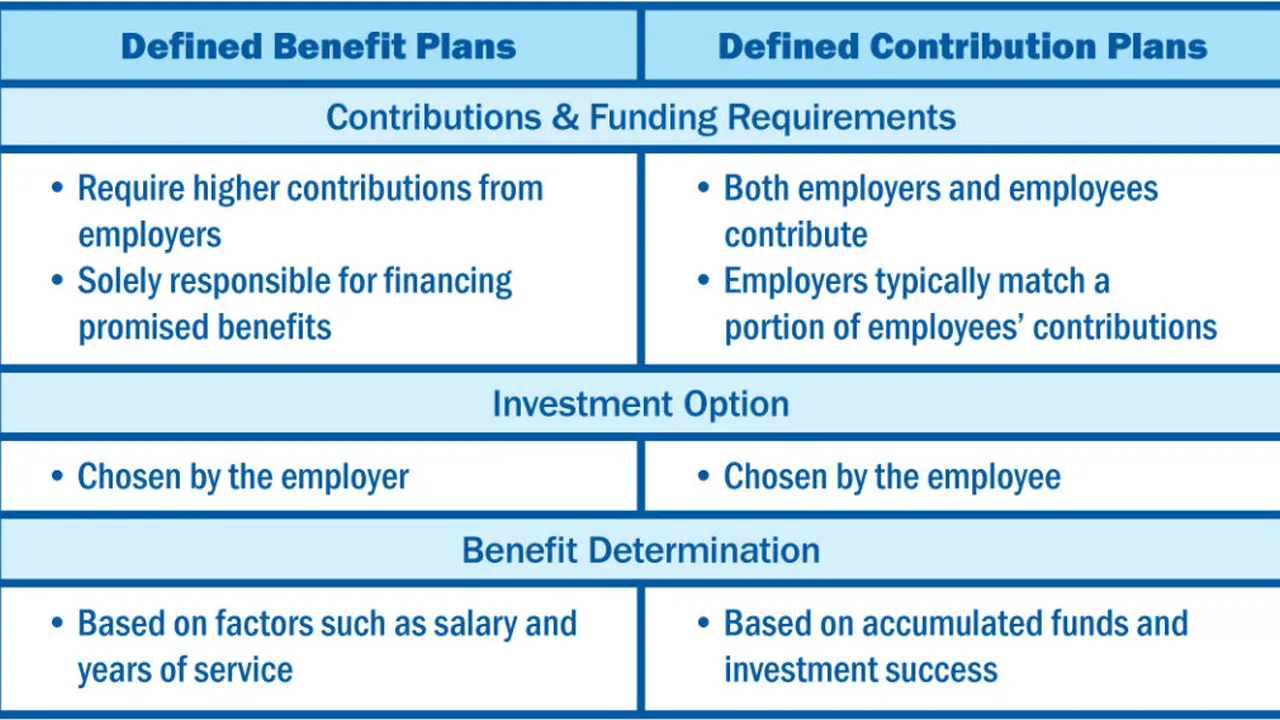

When we talk about traditional pension plans, we're usually referring to what are formally known as 'defined benefit' plans. These plans were once the gold standard for retirement security, especially in large corporations and government sectors. The core promise of a defined benefit plan is that it guarantees a specific payout amount at retirement, typically based on a formula that considers your years of service and your final average salary. It's like a promise from your employer: 'Work for us for X years, earn Y salary, and we'll pay you Z dollars every month for the rest of your life after you retire.'

The employer bears the investment risk in a defined benefit plan. This means they are responsible for ensuring there's enough money in the pension fund to pay out all future retirees. They manage the investments, and if the investments underperform, the company has to make up the difference. This provides a huge sense of security for employees, as they don't have to worry about market fluctuations impacting their retirement income. The benefits are often paid out as a lifetime annuity, meaning you receive regular payments for as long as you live, and sometimes even for your surviving spouse.

Historically, these plans were prevalent because they fostered employee loyalty and provided a stable retirement for a workforce that often stayed with one company for their entire career. However, defined benefit plans have become less common in the private sector due to their high cost and the significant financial risk they impose on employers. Many companies found it increasingly difficult to manage the long-term liabilities associated with these plans, especially with fluctuating interest rates and longer life expectancies.

Exploring Modern Defined Contribution Plans: 401k and IRA

In contrast to defined benefit plans, 'defined contribution' plans have become the dominant retirement savings vehicle in the private sector. The most common examples are 401(k)s, 403(b)s (for non-profits), and Individual Retirement Accounts (IRAs). With these plans, the 'contribution' is defined, not the 'benefit.' This means you (and often your employer) contribute a specific amount of money into an individual account, and the retirement benefit you receive depends entirely on how much you and your employer contribute, and how well your investments perform.

The investment risk in a defined contribution plan shifts from the employer to the employee. You, as the employee, typically choose how your contributions are invested from a selection of options provided by your plan administrator. These options usually include mutual funds, exchange-traded funds (ETFs), and sometimes individual stocks or bonds. If your investments perform well, your retirement nest egg grows. If they perform poorly, your retirement savings could be negatively impacted. This puts the onus on you to make informed investment decisions and monitor your portfolio.

A significant advantage of defined contribution plans is their portability. If you change jobs, you can usually roll over your 401(k) or 403(b) into an IRA or your new employer's plan, allowing your retirement savings to grow continuously regardless of your employment changes. This flexibility is well-suited to today's more mobile workforce.

Employer contributions, often in the form of matching contributions, are a key feature of many defined contribution plans. For example, an employer might match 50% of your contributions up to 6% of your salary. This 'free money' is a powerful incentive to participate and can significantly boost your retirement savings over time. However, unlike defined benefit plans, there's no guaranteed payout; your retirement income will depend on your accumulated savings and how you choose to draw them down (e.g., through systematic withdrawals, annuities purchased with your savings, etc.).

Key Differences and Their Implications for Retirement Planning

Let's break down the core differences between these two types of plans and what they mean for your retirement journey.

Investment Risk and Responsibility: Who Bears the Burden?

In a defined benefit plan, the employer shoulders the investment risk. They are responsible for ensuring the fund has enough money to pay out promised benefits, regardless of market performance. This means less stress for the employee regarding investment decisions. In contrast, with defined contribution plans, you, the employee, bear the investment risk. Your retirement income is directly tied to your investment choices and market performance. This requires you to be more engaged in managing your investments or seeking professional advice.

Guaranteed Income vs Market-Dependent Growth: Predictability vs Potential

Defined benefit plans offer a predictable, often guaranteed, stream of income in retirement, typically for life. This provides a strong sense of financial security. Defined contribution plans, however, offer market-dependent growth. While they have the potential for significant growth if investments perform well, there's no guarantee of a specific income level in retirement. Your income will depend on your accumulated balance and your withdrawal strategy.

Portability and Flexibility: Moving with Your Money

Defined benefit plans are generally less portable. If you leave an employer before retirement, your benefits might be frozen or you might receive a reduced payout. Defined contribution plans are highly portable. You can easily roll over your funds when you change jobs, maintaining continuity in your retirement savings.

Contribution Structure: Employer-Driven vs Employee-Driven

In defined benefit plans, employer contributions are determined by actuarial calculations to meet future benefit obligations. In defined contribution plans, contributions are typically a percentage of your salary, often with employer matching. This gives you more control over how much you contribute and, consequently, how much you save.

Tax Implications: Pre-Tax vs Post-Tax Options

Both types of plans generally offer tax advantages. Defined benefit plan contributions are typically tax-deductible for the employer, and benefits are taxed as ordinary income in retirement. Defined contribution plans like traditional 401(k)s and IRAs allow pre-tax contributions to grow tax-deferred, with withdrawals taxed in retirement. Roth 401(k)s and Roth IRAs allow after-tax contributions to grow tax-free, with qualified withdrawals also tax-free in retirement. The choice between pre-tax and post-tax options depends on your current and future tax situation.

Specific Product Recommendations and Use Cases

Since defined contribution plans are the most common for individual management, let's dive into some specific products and their use cases, along with typical costs.

401(k) Plans: Employer-Sponsored Retirement Savings

Use Case: Ideal for employees whose employers offer a 401(k) plan, especially if there's an employer match. This is often the first and most important retirement savings vehicle for many working individuals.

Key Features:

- Contribution Limits: For 2024, you can contribute up to $23,000 ($30,500 if age 50 or older) to a 401(k).

- Employer Match: Many employers offer a matching contribution, which is essentially 'free money' for your retirement. Always contribute at least enough to get the full match.

- Investment Options: Typically offers a curated list of mutual funds, target-date funds, and sometimes ETFs.

- Loan Options: Some 401(k) plans allow you to borrow from your account, though this should be a last resort.

- Traditional vs Roth: Many plans offer both traditional (pre-tax) and Roth (after-tax) 401(k) options.

Typical Costs: Fees vary widely depending on the plan administrator and the investment options. These can include administrative fees (often paid by the employer but sometimes passed to employees), record-keeping fees, and expense ratios of the underlying funds. Expense ratios for mutual funds in 401(k)s can range from 0.05% for index funds to over 1% for actively managed funds. It's crucial to check your plan's fee disclosure statement.

Recommended Providers (for employers, as individuals don't choose the provider): Large providers like Fidelity, Vanguard, Charles Schwab, and Empower Retirement are common. They offer robust platforms and a wide range of investment options for employers to choose from.

Individual Retirement Accounts (IRAs): Personal Retirement Savings

Use Case: Excellent for anyone with earned income, especially if you don't have access to a 401(k) or want to supplement your employer-sponsored plan. IRAs offer more investment flexibility than most 401(k)s.

Key Features:

- Contribution Limits: For 2024, you can contribute up to $7,000 ($8,000 if age 50 or older) to an IRA.

- Traditional IRA: Contributions may be tax-deductible, and earnings grow tax-deferred. Withdrawals are taxed in retirement.

- Roth IRA: Contributions are made with after-tax dollars, but qualified withdrawals in retirement are tax-free. Ideal if you expect to be in a higher tax bracket in retirement.

- Investment Flexibility: You can invest in almost anything: stocks, bonds, mutual funds, ETFs, real estate (through a self-directed IRA), etc.

Typical Costs: Generally lower than 401(k)s as you choose your own brokerage. Brokerage firms often charge no annual fees for IRAs. Investment costs come from the expense ratios of the funds you choose (e.g., 0.03% for a Vanguard S&P 500 ETF, 0.50% for an actively managed mutual fund) or trading commissions if you buy individual stocks (many brokers now offer commission-free stock and ETF trading).

Recommended Providers:

- Vanguard: Known for low-cost index funds and ETFs. Great for a hands-off, diversified approach.

- Fidelity: Offers a wide range of investment products, including their own zero-expense-ratio index funds. Strong research tools.

- Charles Schwab: Similar to Fidelity, with a broad selection of investments and good customer service.

- M1 Finance: Good for automated investing with custom portfolios and fractional shares.

- Betterment/Wealthfront (Robo-Advisors): If you prefer a completely hands-off approach, these robo-advisors manage your IRA for a small fee (e.g., 0.25% - 0.40% of assets under management per year), investing in diversified ETFs.

SEP IRA and SIMPLE IRA: Small Business Retirement Solutions

Use Case: Designed for self-employed individuals and small business owners to save for retirement and offer plans to their employees.

SEP IRA (Simplified Employee Pension):

- Use Case: Best for self-employed individuals or small businesses with few or no employees. Easy to set up and administer.

- Contribution Limits: For 2024, you can contribute up to 25% of your compensation (or 20% of net earnings from self-employment) up to $69,000. Only employer contributions are allowed.

- Flexibility: Contributions can vary year to year, making it flexible for businesses with fluctuating income.

SIMPLE IRA (Savings Incentive Match Plan for Employees):

- Use Case: Suitable for small businesses with 100 or fewer employees. Simpler to administer than a 401(k).

- Contribution Limits: For 2024, employees can contribute up to $16,000 ($19,500 if age 50 or older). Employers must either match employee contributions up to 3% of salary or make a 2% non-elective contribution for all eligible employees.

- Mandatory Employer Contributions: Unlike SEP IRAs, employer contributions are mandatory.

Typical Costs: Similar to individual IRAs, costs depend on the chosen brokerage and underlying investments. Administrative fees are generally low or non-existent for SEP/SIMPLE IRAs at major brokerages.

Recommended Providers: Vanguard, Fidelity, Charles Schwab, and other major brokerage firms offer SEP and SIMPLE IRA accounts.

Choosing the Right Plan: A Decision Framework

Deciding between different retirement plans, or how to prioritize them, depends on your employment situation, income level, and financial goals.

For Employees with a 401(k) Match: Prioritize the Free Money

If your employer offers a 401(k) with a matching contribution, your first priority should almost always be to contribute at least enough to get the full match. This is an immediate, guaranteed return on your investment that you won't find anywhere else. For example, if your employer matches 50% of your contributions up to 6% of your salary, contributing 6% of your salary means you're getting an instant 50% return on that portion of your savings.

Maximizing Tax Advantages: Traditional vs Roth

Once you've secured any employer match, consider whether a traditional (pre-tax) or Roth (after-tax) account is better for you. If you expect to be in a higher tax bracket now than in retirement, a traditional 401(k) or IRA might be better, as you get a tax deduction now. If you expect to be in a higher tax bracket in retirement, or if you're currently in a low tax bracket, a Roth 401(k) or Roth IRA could be more advantageous, as your qualified withdrawals will be tax-free in retirement.

Diversifying Your Retirement Accounts: Beyond the Basics

It's often beneficial to have a mix of traditional and Roth accounts to provide tax flexibility in retirement. For example, you might contribute to your traditional 401(k) for the employer match and then contribute to a Roth IRA for additional tax-free growth. If you max out your 401(k) and IRA contributions, consider a taxable brokerage account for additional investment growth, though these don't offer the same tax advantages.

Self-Employed and Small Business Owners: Tailored Solutions

If you're self-employed, a SEP IRA or Solo 401(k) can allow for much higher contribution limits than a traditional or Roth IRA. A Solo 401(k) can be particularly powerful as it allows you to contribute both as an employee and as an employer. For small businesses with employees, a SIMPLE IRA is a good stepping stone before considering a full-fledged 401(k) due to its simpler administration.

The Evolution of Retirement Planning: Adapting to Change

The shift from defined benefit to defined contribution plans reflects a broader change in the economic landscape and the nature of employment. While defined benefit plans offered unparalleled security, they became unsustainable for many private companies. Defined contribution plans, while placing more responsibility on the individual, offer greater flexibility, portability, and the potential for significant wealth accumulation through personal investment choices.

Understanding the nuances of each plan type is crucial for effective retirement planning. Whether you're relying on an employer-sponsored 401(k), managing your own IRA, or running a small business, making informed decisions about your retirement savings vehicles is paramount to building a secure financial future. Regularly review your contributions, investment choices, and overall retirement strategy to ensure you're on track to meet your goals.

:max_bytes(150000):strip_icc()/277019-baked-pork-chops-with-cream-of-mushroom-soup-DDMFS-beauty-4x3-BG-7505-5762b731cf30447d9cbbbbbf387beafa.jpg)