Evaluate the differences between traditional and Roth retirement accounts to choose the best tax strategy for your future.

Evaluate the differences between traditional and Roth retirement accounts to choose the best tax strategy for your future.

Comparing Traditional vs Roth Retirement Accounts

Understanding Retirement Account Basics

Alright, let's dive into the nitty-gritty of retirement accounts. When you're thinking about saving for your golden years, two big players usually pop up: Traditional IRAs/401(k)s and Roth IRAs/401(k)s. They both help you save for retirement, but they do it in fundamentally different ways, especially when it comes to taxes. And let's be real, taxes can make a huge difference in how much money you actually get to keep when you retire. So, understanding these differences is super important for making smart financial moves.

Think of it like this: one is 'pay taxes now, enjoy tax-free later,' and the other is 'defer taxes now, pay taxes later.' Which one is better for you really depends on your current income, what you expect your income to be in retirement, and your overall financial philosophy. It's not a one-size-fits-all kind of deal, and that's why we're going to break it all down.

Traditional Retirement Accounts Tax Benefits

Let's kick things off with Traditional retirement accounts. This includes Traditional IRAs and Traditional 401(k)s. The main draw here is the upfront tax deduction. When you contribute to a Traditional IRA or 401(k), those contributions are often tax-deductible in the year you make them. This means your taxable income for that year goes down, which can lead to a lower tax bill right now. Pretty sweet, right?

For example, if you earn $70,000 a year and contribute $6,000 to a Traditional IRA, your taxable income could drop to $64,000. This immediate tax break is a big reason why many people opt for Traditional accounts, especially if they're in a higher tax bracket today.

But here's the flip side: your money grows tax-deferred. This means you don't pay taxes on the investment gains year after year. That's fantastic for compounding your returns. However, when you start taking distributions in retirement, those withdrawals are taxed as ordinary income. So, you're essentially pushing your tax bill down the road.

This strategy is generally favored by folks who believe they're in a higher tax bracket now than they will be in retirement. If you're earning a lot today and expect to be in a lower tax bracket when you're retired (maybe because you'll have less income, or tax rates might be lower), then deferring those taxes makes a lot of sense.

Roth Retirement Accounts Tax Advantages

Now, let's flip the coin and talk about Roth retirement accounts. This includes Roth IRAs and Roth 401(k)s. The big difference here is when you get your tax break. With Roth accounts, your contributions are made with after-tax dollars. This means you don't get an upfront tax deduction like you do with Traditional accounts. So, your current taxable income isn't reduced.

However, the magic happens in retirement. All qualified withdrawals from a Roth account are completely tax-free. Yes, you heard that right – tax-free! This includes all your contributions and all the investment earnings. Imagine having a big chunk of money in retirement that you don't have to worry about Uncle Sam taking a slice of. That's the power of Roth.

To qualify for tax-free withdrawals, your Roth IRA must be open for at least five years, and you must be at least 59½ years old, disabled, or using the money for a first-time home purchase (up to $10,000). For Roth 401(k)s, similar rules apply.

Roth accounts are particularly attractive to younger individuals who are likely in a lower tax bracket now but expect to be in a higher tax bracket in the future. If you anticipate your income growing significantly over your career, or if you believe tax rates will be higher in the future, then paying taxes now at a lower rate and enjoying tax-free income later is a very compelling strategy.

Contribution Limits and Income Restrictions

Both Traditional and Roth accounts have contribution limits, which are set by the IRS and can change annually. It's super important to stay updated on these limits to maximize your savings.

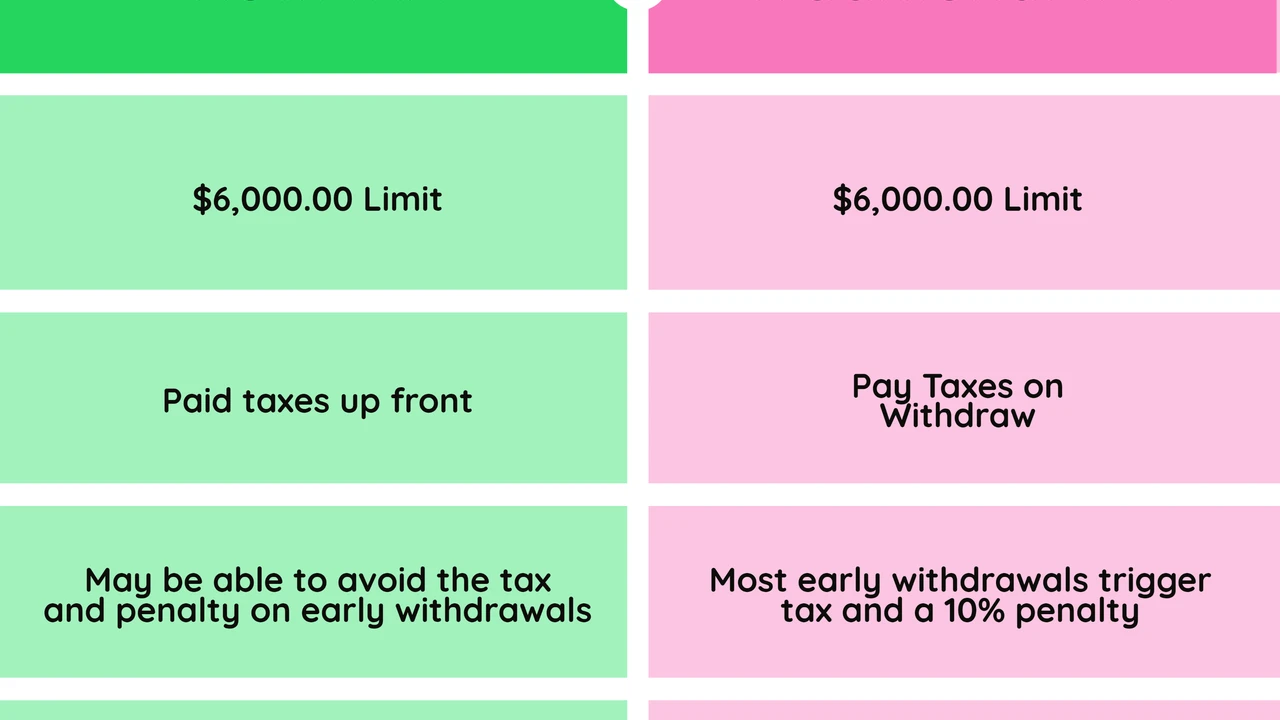

For 2024, the IRA contribution limit is $7,000, or $8,000 if you're age 50 or over (this extra $1,000 is called a catch-up contribution). These limits apply to your combined contributions to all your Traditional and Roth IRAs. So, you can't put $7,000 into a Traditional IRA and another $7,000 into a Roth IRA in the same year.

Now, here's where Roth IRAs get a bit tricky: they have income limitations. If your modified adjusted gross income (MAGI) is above a certain threshold, you might not be able to contribute directly to a Roth IRA, or your contribution might be limited. For 2024, if you're a single filer, the ability to contribute to a Roth IRA begins to phase out at a MAGI of $146,000 and is eliminated at $161,000. For married couples filing jointly, the phase-out begins at $230,000 and is eliminated at $240,000.

But don't despair if you're a high earner! There's a workaround called the 'backdoor Roth IRA.' This involves contributing non-deductible money to a Traditional IRA and then immediately converting it to a Roth IRA. It's a perfectly legal strategy, but it can be a bit complex, especially if you have existing Traditional IRA balances. Always a good idea to chat with a financial advisor if you're considering this.

For 401(k)s (both Traditional and Roth), the contribution limits are much higher. For 2024, you can contribute up to $23,000, or $30,500 if you're age 50 or over. The great news is that there are no income limitations for contributing to a Roth 401(k) through your employer, which makes it a fantastic option for high earners who are locked out of direct Roth IRA contributions.

Withdrawal Rules and Flexibility

Understanding when and how you can access your money is crucial. Both Traditional and Roth accounts have rules about withdrawals, especially before retirement age.

For Traditional IRAs and 401(k)s, withdrawals before age 59½ are generally subject to a 10% early withdrawal penalty, in addition to being taxed as ordinary income. There are some exceptions, like for certain medical expenses, higher education costs, or a first-time home purchase (up to $10,000 from an IRA). But generally, you want to leave that money untouched until retirement.

Another important rule for Traditional accounts is Required Minimum Distributions (RMDs). Once you reach a certain age (currently 73, but it's been changing), the IRS requires you to start taking money out of your Traditional IRA and 401(k)s, whether you need it or not. This is because the government wants to collect those deferred taxes. If you don't take your RMD, there's a hefty penalty.

Roth accounts offer a lot more flexibility when it comes to withdrawals. Since your contributions were already taxed, you can withdraw your original contributions at any time, tax-free and penalty-free, regardless of your age or how long the account has been open. This is a huge advantage, as it means your Roth IRA can act as a sort of emergency fund or a flexible savings vehicle if needed.

For the earnings in a Roth account, they become tax-free and penalty-free after the account has been open for five years and you meet one of the qualifying conditions (age 59½, disability, or first-time home purchase). Unlike Traditional accounts, Roth IRAs do not have RMDs for the original owner. This means you can leave the money in your Roth IRA to continue growing tax-free for as long as you want, and even pass it on to your heirs tax-free. Roth 401(k)s do have RMDs, but you can roll them over into a Roth IRA to avoid RMDs.

Choosing the Right Account for Your Future

So, how do you decide which one is right for you? It really boils down to your current tax situation versus your expected tax situation in retirement. Here's a simple way to think about it:

* **Choose Traditional if:** You expect to be in a lower tax bracket in retirement than you are now. You want an immediate tax deduction to lower your current tax bill. You're not worried about RMDs or prefer to defer taxes as long as possible.

* **Choose Roth if:** You expect to be in a higher tax bracket in retirement than you are now. You prefer tax-free income in retirement. You want the flexibility to withdraw contributions tax-free and penalty-free before retirement. You want to avoid RMDs (with a Roth IRA).

Many people actually use a combination of both Traditional and Roth accounts. This strategy, often called 'tax diversification,' can be very powerful. By having both pre-tax and after-tax money in retirement, you give yourself more flexibility to manage your tax burden in the future. For example, in retirement, you might withdraw from your Traditional account up to a certain tax bracket, and then switch to your Roth account for tax-free income, effectively controlling your taxable income each year.

Specific Product Recommendations and Platforms

Alright, let's get practical. Where can you actually open these accounts and what platforms are good for managing them? There are tons of options out there, from big-name brokerages to newer fintech platforms. Here are a few popular choices, keeping in mind that fees, investment options, and user experience can vary.

Fidelity Investments

Fidelity is a giant in the investment world, and for good reason. They offer a wide range of investment products, including Traditional and Roth IRAs, and they're often the provider for employer-sponsored 401(k)s. Their platform is robust, offering extensive research tools, educational resources, and a huge selection of mutual funds, ETFs, and individual stocks. They also have a strong customer service team.

* **Pros:** Wide selection of investment options, low-cost index funds and ETFs, excellent research tools, strong customer support, no account minimums for IRAs.

* **Cons:** The sheer volume of options can be overwhelming for beginners.

* **Typical Fees:** Many commission-free ETFs and stocks. Fidelity's own index funds often have zero expense ratios. Other mutual funds will have their own expense ratios.

* **Use Case:** Great for both beginners and experienced investors who want a comprehensive platform with lots of choices and research capabilities.

Vanguard

Vanguard is famous for its low-cost index funds and ETFs, which are a favorite among passive investors. If you're looking to keep your investment costs down, Vanguard is definitely a top contender. They offer Traditional and Roth IRAs, and their platform is straightforward, focusing on long-term, low-cost investing.

* **Pros:** Industry leader in low-cost index funds and ETFs, strong commitment to investor-first philosophy, simple and effective platform.

* **Cons:** Less emphasis on active trading tools or individual stock research compared to some competitors. Customer service can sometimes be slower due to high demand.

* **Typical Fees:** Very low expense ratios on their proprietary funds. Commission-free trading for Vanguard ETFs.

* **Use Case:** Ideal for long-term investors who prioritize low costs and a simple, diversified investment approach, especially those interested in index funds.

Charles Schwab

Charles Schwab is another well-established brokerage firm that offers a full suite of financial services, including Traditional and Roth IRAs. They've been very competitive on fees, offering commission-free stock and ETF trading. Their platform is user-friendly, and they provide a good balance of research, educational content, and investment options.

* **Pros:** Commission-free trading for stocks and ETFs, good selection of mutual funds, strong customer service, user-friendly platform, extensive branch network if you prefer in-person support.

* **Cons:** Some might find their research tools not as in-depth as Fidelity's for certain niche areas.

* **Typical Fees:** Commission-free stock and ETF trading. Expense ratios on mutual funds vary.

* **Use Case:** Excellent for investors who want a reliable, full-service brokerage with competitive pricing and a good range of investment choices.

M1 Finance

M1 Finance is a bit different. It's a hybrid platform that combines automated investing (like a robo-advisor) with the flexibility of self-directed investing. You build a 'pie' of investments (stocks and ETFs), and M1 automatically invests your money according to your chosen allocations. They offer Traditional and Roth IRAs.

* **Pros:** Automated investing with customization, no management fees for basic accounts, fractional shares (allowing you to invest small amounts into expensive stocks), intuitive interface.

* **Cons:** Less control over individual trades (it's designed for long-term, hands-off investing), not ideal for active traders.

* **Typical Fees:** No management fees for standard accounts. Premium features (M1 Plus) have a subscription fee. Expense ratios on underlying ETFs apply.

* **Use Case:** Great for investors who want a hands-off approach to building a diversified portfolio but still want some control over their asset allocation. Good for those who like automation but want to pick their own investments.

Betterment / Wealthfront (Robo-Advisors)

If you're looking for a truly hands-off approach, robo-advisors like Betterment and Wealthfront are fantastic. They build and manage a diversified portfolio for you based on your risk tolerance and financial goals. They handle rebalancing, tax-loss harvesting, and dividend reinvestment automatically. Both offer Traditional and Roth IRAs.

* **Pros:** Fully automated investing, low management fees, tax-loss harvesting (can save you money on taxes), diversified portfolios, easy to set up and use.

* **Cons:** Less control over individual investments, limited customization compared to traditional brokerages.

* **Typical Fees:** Management fees typically range from 0.25% to 0.40% of assets under management per year. Expense ratios on underlying ETFs apply.

* **Use Case:** Perfect for beginners or busy individuals who want a professionally managed, diversified portfolio without having to do any of the heavy lifting themselves.

When choosing a platform, consider what's most important to you: low fees, specific investment options, ease of use, customer support, or advanced tools. Many platforms allow you to open both Traditional and Roth IRAs, so you can implement a tax diversification strategy if that's your goal.

Real-World Scenarios and Practical Application

Let's look at a couple of scenarios to see how these choices play out in real life.

**Scenario 1: The Young Professional**

Meet Sarah, 28 years old, just started her career, earning $60,000 a year. She expects her income to grow significantly over the next 10-15 years. She's currently in a relatively low tax bracket. For Sarah, a **Roth 401(k)** (if offered by her employer) and/or a **Roth IRA** would likely be the best choice. She pays taxes now at her current lower rate, and all her growth and withdrawals in retirement will be tax-free. This is a huge advantage if she ends up in a much higher tax bracket later in life.

**Scenario 2: The Mid-Career High Earner**

Now, consider David, 45 years old, earning $150,000 a year. He's in a higher tax bracket now and wants to reduce his current taxable income. He also anticipates that his income might be lower in retirement, or that tax rates might not be significantly higher than they are today. For David, contributing to a **Traditional 401(k)** (especially if his employer offers a match) and potentially a **Traditional IRA** (if he qualifies for the deduction) makes a lot of sense. He gets the immediate tax break, and his money grows tax-deferred. He'll pay taxes in retirement, but hopefully at a lower rate.

**Scenario 3: The Tax Diversifier**

Then there's Emily, 35 years old, earning $90,000. She's not sure what her tax situation will be in retirement, and she wants flexibility. Emily decides to contribute to both a **Traditional 401(k)** (to get her employer match and some upfront tax deduction) and a **Roth IRA** (to build a bucket of tax-free money for retirement). This way, she's hedging her bets against future tax rate changes and gives herself options when she starts withdrawing funds in retirement. She can strategically pull from either account to manage her taxable income each year.

It's important to remember that your financial situation isn't static. What's best for you today might change in five or ten years. It's a good idea to review your retirement strategy periodically, especially after major life events like a significant raise, marriage, or having children. And hey, if you're ever feeling overwhelmed, talking to a qualified financial advisor can provide personalized guidance tailored to your unique circumstances. They can help you navigate the complexities and make sure you're on the right track for a comfortable retirement.

:max_bytes(150000):strip_icc()/277019-baked-pork-chops-with-cream-of-mushroom-soup-DDMFS-beauty-4x3-BG-7505-5762b731cf30447d9cbbbbbf387beafa.jpg)