Understanding Inflation's Impact on Retirement

Learn how inflation can affect your retirement savings and strategies to mitigate its impact.

Learn how inflation can affect your retirement savings and strategies to mitigate its impact.

Understanding Inflation's Impact on Retirement

What is Inflation and Why Does it Matter for Your Retirement?

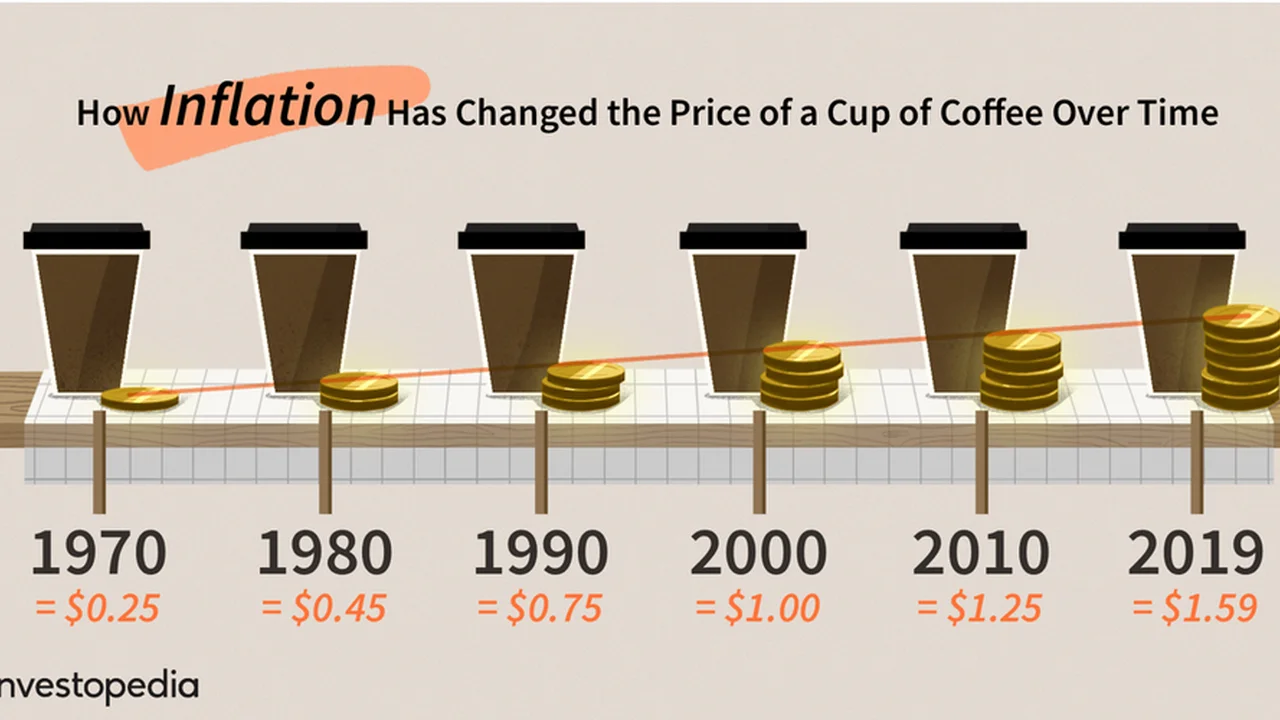

Hey there, future retiree! Ever wonder why a candy bar that cost a dime when your grandparents were kids now costs a dollar or more? That, my friend, is inflation in action. Simply put, inflation is the rate at which the general level of prices for goods and services is rising, and consequently, the purchasing power of currency is falling. Think about it: if your money buys less tomorrow than it does today, that's a big deal, especially when you're planning for a future where you won't have a regular paycheck coming in.

For your retirement savings, inflation isn't just a minor annoyance; it's a silent wealth killer. It erodes the value of your hard-earned money over time. What seems like a comfortable nest egg today might feel pretty meager 20 or 30 years down the line if inflation isn't accounted for. Imagine saving $1 million for retirement. Sounds great, right? But if inflation averages 3% per year, that $1 million will only have the purchasing power of about $550,000 in 20 years. That's a huge chunk of your future lifestyle gone, just like that. Understanding this fundamental concept is the first step in building a truly resilient retirement plan.

How Inflation Erodes Your Retirement Savings Purchasing Power

Let's dive a bit deeper into how this erosion happens. When prices go up, your fixed income or savings that aren't growing at least as fast as inflation lose value. Consider your daily expenses: groceries, utilities, healthcare, transportation, and leisure activities. All these costs tend to rise over time. If your retirement income doesn't keep pace, you'll find yourself cutting back on things you once enjoyed or even struggling to cover basic necessities. This is particularly critical for healthcare costs, which historically tend to inflate at a higher rate than general consumer prices. A medical procedure that costs $10,000 today could easily be $20,000 or more in 15-20 years. Without proper planning, your retirement healthcare budget could be completely blown.

Another aspect is the 'sequence of returns risk' combined with inflation. If you experience a market downturn early in your retirement, and inflation is high, you're essentially selling your assets at a lower price while everything costs more. This double whammy can significantly deplete your principal, making it harder for your portfolio to recover and sustain you throughout your retirement years. It's not just about having enough money; it's about having enough money that buys enough.

Strategies to Mitigate Inflation's Impact on Your Retirement Portfolio

Alright, so inflation is a beast. But you're not helpless! There are several powerful strategies you can employ to fight back and protect your retirement nest egg. It's all about making your money work harder than inflation.

Investing in Inflation Protected Securities TIPS and I Bonds

One of the most direct ways to combat inflation is to invest in assets specifically designed to protect against it. Treasury Inflation-Protected Securities (TIPS) and I Bonds are two excellent options issued by the U.S. Treasury.

Treasury Inflation Protected Securities TIPS

TIPS are a type of Treasury bond that provides protection against inflation. The principal value of a TIPS increases with inflation and decreases with deflation, as measured by the Consumer Price Index (CPI). When a TIPS matures, you receive either the original or adjusted principal, whichever is greater. You also receive interest payments twice a year, which are calculated based on the adjusted principal. This means both your principal and your interest payments adjust with inflation, giving you a real return.

Usage Scenario: TIPS are great for conservative investors who want to ensure their principal's purchasing power is preserved. They are often used as a component of a diversified portfolio, especially for those nearing or in retirement who prioritize capital preservation over aggressive growth. They can be purchased directly from TreasuryDirect or through a brokerage account.

Product Comparison:

- Vanguard Inflation-Protected Securities Fund (VIPSX): An actively managed mutual fund that invests in TIPS. Expense Ratio: 0.20%. Minimum Investment: $3,000.

- iShares TIPS Bond ETF (TIP): An exchange-traded fund (ETF) that tracks an index of TIPS. Expense Ratio: 0.19%. Can be bought and sold like stocks, no minimum investment beyond the share price.

- Schwab U.S. TIPS ETF (SCHP): Another popular TIPS ETF. Expense Ratio: 0.03%. Very low cost.

Pricing: ETFs like TIP and SCHP trade at market prices, which fluctuate. Mutual funds like VIPSX have a net asset value (NAV) that updates daily. Direct purchases from TreasuryDirect are at auction prices.

Series I Savings Bonds I Bonds

I Bonds are another fantastic inflation-fighting tool. They earn interest based on a combination of a fixed rate (which stays the same for the life of the bond) and a variable inflation rate (which changes every six months). This means your interest rate adjusts to keep pace with inflation, ensuring your money maintains its purchasing power. You can buy up to $10,000 in electronic I Bonds per calendar year per Social Security number, plus an additional $5,000 in paper I Bonds with your tax refund.

Usage Scenario: I Bonds are ideal for short-to-medium term savings goals (though they can be held for 30 years) and for building an emergency fund that won't lose value to inflation. They are extremely safe, backed by the U.S. government, and offer tax advantages (interest is tax-deferred until redemption and exempt from state/local income taxes). You must hold them for at least one year, and if you redeem them within five years, you forfeit the last three months of interest.

Product Comparison: I Bonds are purchased directly from TreasuryDirect. There are no third-party products. Their appeal lies in their simplicity and direct inflation protection.

Pricing: Purchased at face value (e.g., a $100 I Bond costs $100).

Diversifying Your Portfolio with Real Assets and Equities

Beyond direct inflation protection, a well-diversified portfolio is your best friend. Certain asset classes tend to perform better during inflationary periods.

Real Estate and REITs for Inflation Hedging

Real estate often acts as a natural hedge against inflation. As inflation rises, so do property values and rental income. This means your real estate investments can appreciate in value and generate higher income streams, helping to offset rising costs. You don't have to buy physical properties to benefit; Real Estate Investment Trusts (REITs) offer a liquid way to invest in real estate.

Usage Scenario: REITs are suitable for investors looking for exposure to real estate without the hassle of direct property ownership. They can provide both income (through dividends) and capital appreciation. They are a good addition to a diversified portfolio for long-term growth and inflation protection.

Product Comparison:

- Vanguard Real Estate Index Fund ETF (VNQ): A popular ETF that invests in a broad range of REITs. Expense Ratio: 0.12%.

- Schwab U.S. REIT ETF (SCHH): Another low-cost REIT ETF. Expense Ratio: 0.07%.

- Fidelity Real Estate Index Fund (FSRNX): A mutual fund option. Expense Ratio: 0.07%. Minimum Investment: $0.

Pricing: ETFs trade at market prices. Mutual funds have NAVs.

Commodities and Natural Resources for Inflation Protection

Commodities like oil, gold, silver, and agricultural products tend to perform well when inflation is on the rise because their prices are directly tied to the cost of goods. Investing in commodity-linked ETFs or mutual funds can provide this exposure.

Usage Scenario: Commodities can be a small but effective part of a diversified portfolio to hedge against inflation. They are generally more volatile than other asset classes, so a smaller allocation is often recommended.

Product Comparison:

- Invesco DB Commodity Index Tracking Fund (DBC): An ETF that tracks a diversified basket of commodities. Expense Ratio: 0.88%.

- SPDR Gold Shares (GLD): An ETF that holds physical gold. Expense Ratio: 0.40%.

- Aberdeen Standard Physical Silver Shares ETF (SIVR): An ETF that holds physical silver. Expense Ratio: 0.30%.

Pricing: ETFs trade at market prices.

Equities Stocks and Growth Potential

Historically, stocks have been one of the best long-term hedges against inflation. Companies can often pass on increased costs to consumers through higher prices, which can lead to increased revenues and profits. Investing in companies with strong pricing power, low debt, and consistent earnings growth can be particularly effective.

Usage Scenario: A core component of any long-term retirement portfolio. Focus on diversified index funds or ETFs that track broad market indices, as well as individual companies with strong fundamentals.

Product Comparison:

- Vanguard Total Stock Market Index Fund ETF (VTI): Tracks the entire U.S. stock market. Expense Ratio: 0.03%.

- SPDR S&P 500 ETF Trust (SPY): Tracks the S&P 500 index. Expense Ratio: 0.09%.

- Fidelity ZERO Total Market Index Fund (FZROX): A zero-expense ratio mutual fund tracking the total U.S. stock market. Minimum Investment: $0.

Pricing: ETFs trade at market prices. Mutual funds have NAVs.

Considering Annuities and Other Income Streams

While not always popular, certain types of annuities can offer inflation protection, especially those with inflation riders or variable components.

Inflation-Adjusted Annuities for Guaranteed Income

Some annuities offer riders that increase your payments over time to keep pace with inflation. While these riders come at an additional cost, they can provide peace of mind that your guaranteed income stream won't be eroded by rising prices.

Usage Scenario: Suitable for individuals who prioritize a guaranteed income stream in retirement and are willing to pay for inflation protection. Best considered as a portion of your overall retirement income strategy, not the sole source.

Product Comparison: Annuities are complex and vary widely by provider. It's crucial to work with a qualified financial advisor to compare specific products from companies like:

- New York Life: Offers various annuity products, including those with inflation riders.

- Fidelity: Provides a range of annuity options.

- Jackson National Life: Known for its variable annuity offerings.

Pricing: Annuity costs vary significantly based on the type, features, and riders chosen. Expect surrender charges if you withdraw money early.

Reviewing Your Retirement Withdrawal Strategy

How you withdraw money from your retirement accounts also plays a huge role in combating inflation. A static withdrawal rate might not cut it.

Dynamic Withdrawal Strategies for Flexibility

Instead of a fixed 4% withdrawal rule, consider a dynamic strategy where you adjust your withdrawals based on market performance and inflation. In years of high inflation or poor market returns, you might withdraw less, and in good years, you might take a bit more. This flexibility helps your portfolio last longer.

Usage Scenario: For retirees who are comfortable with some variability in their annual income and want to maximize the longevity of their portfolio. This requires active monitoring and adjustment.

Product Comparison: This is more of a strategy than a product. Financial planning software can help model different withdrawal scenarios. Examples include:

- Personal Capital (now Empower Personal Wealth): Offers free financial planning tools and paid advisory services.

- NewRetirement: A comprehensive retirement planning platform with advanced withdrawal modeling. Subscription fees apply (e.g., $120/year for PlannerPlus).

- Fidelity's Retirement Planning Tools: Free tools for Fidelity customers to model various scenarios.

Pricing: Free tools are available, but more advanced features or advisory services come with fees.

The Importance of Regular Portfolio Review and Adjustment

Inflation isn't a one-time event; it's an ongoing economic force. That's why your retirement plan can't be a 'set it and forget it' deal. You need to regularly review your portfolio, at least once a year, to ensure it's still aligned with your goals and effectively combating inflation. Are your inflation-protected assets still performing as expected? Do you need to rebalance your equity exposure? Are your income streams keeping pace with rising costs?

Life changes, market conditions shift, and inflation rates fluctuate. Being proactive and making necessary adjustments will be key to maintaining your purchasing power throughout your retirement. Don't be afraid to consult with a financial advisor who specializes in retirement planning. They can provide personalized guidance and help you navigate the complexities of inflation-proofing your golden years. Remember, your future self will thank you for the effort you put in today!

:max_bytes(150000):strip_icc()/277019-baked-pork-chops-with-cream-of-mushroom-soup-DDMFS-beauty-4x3-BG-7505-5762b731cf30447d9cbbbbbf387beafa.jpg)