Understanding the Power of Compound Interest in Savings

{ "article": [ { "title": "Understanding the Power of Compound Interest in Savings", "meta_description": "Learn how compound interest can dramatically accelerate your savings growth over time.", "content": "Learn how compound interest can dramatically accelerate your savings growth over time.\n\n

\n\n

Compound Interest Explained Your Money's Best Friend

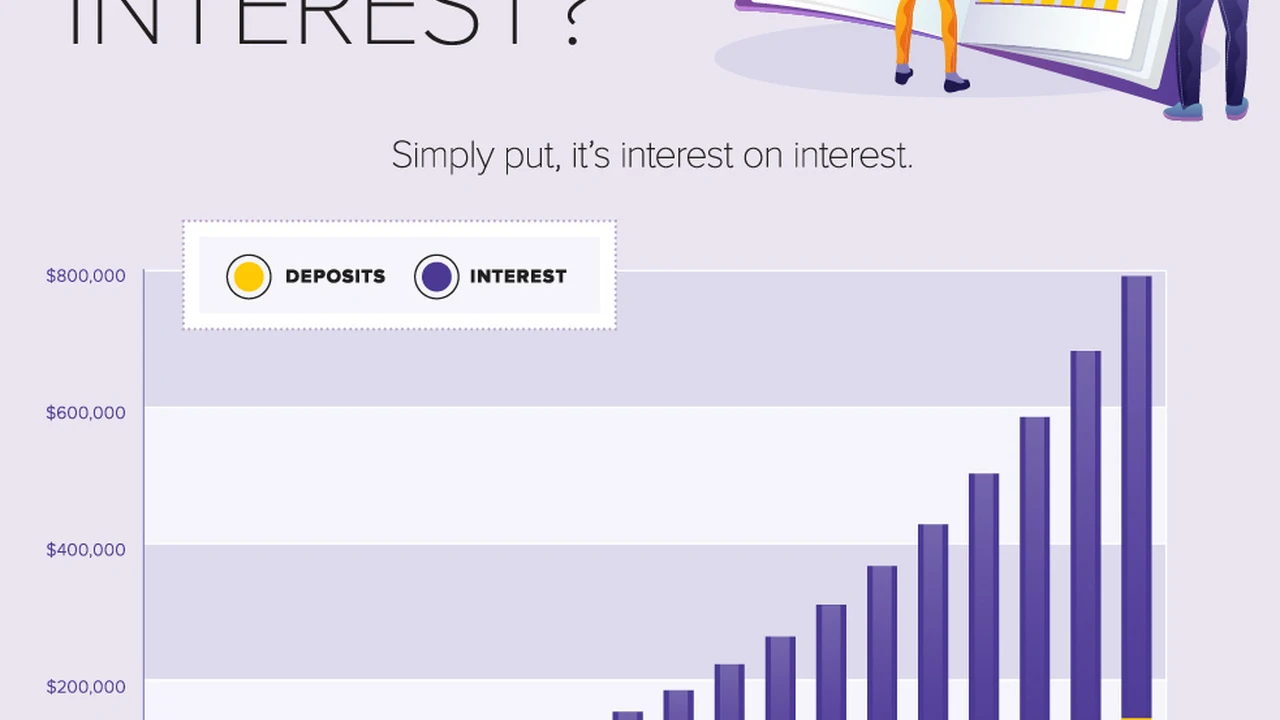

\n\nHey there, money-savvy folks! Ever heard the phrase, “The eighth wonder of the world is compound interest”? Albert Einstein supposedly said that, and for good reason. Compound interest is seriously powerful. It’s not just about earning interest on your initial money; it’s about earning interest on your interest. Think of it like a snowball rolling downhill – it just keeps getting bigger and bigger. This concept is absolutely fundamental to growing your wealth, whether you're saving for a down payment, retirement, or just building up your emergency fund.

\n\nLet's break it down. Simple interest is straightforward: you earn interest only on the original principal amount. Compound interest, however, takes the interest you've already earned and adds it to your principal. Then, in the next period, you earn interest on that new, larger principal. This cycle repeats, creating an exponential growth effect. The longer your money is invested, and the more frequently the interest compounds (daily, monthly, quarterly, annually), the more dramatic the effect.

\n\nThe Mechanics of Compounding How Your Savings Multiply

\n\nSo, how does this magic happen? Let's use a simple example. Imagine you invest $1,000 at an annual interest rate of 5%. With simple interest, you'd earn $50 each year. After 10 years, you'd have your original $1,000 plus $500 in interest, totaling $1,500.

\n\nNow, let's apply compound interest. In the first year, you still earn $50. But in the second year, you earn 5% on $1,050 (your original $1,000 plus the $50 interest). That's $52.50. In the third year, you earn 5% on $1,102.50, and so on. While the difference might seem small initially, over time, it becomes significant. After 10 years, with annual compounding, your $1,000 would grow to approximately $1,628.89. That's an extra $128.89 just from the power of compounding!

\n\nThe formula for compound interest is A = P(1 + r/n)^(nt), where:

\n- \n

- A = the future value of the investment/loan, including interest \n

- P = the principal investment amount (the initial deposit or loan amount) \n

- r = the annual interest rate (as a decimal) \n

- n = the number of times that interest is compounded per year \n

- t = the number of years the money is invested or borrowed for \n

Don't worry if the formula looks intimidating. The key takeaway is that time and the frequency of compounding are your best friends. The earlier you start saving, and the more often your interest compounds, the better.

\n\nReal-World Applications of Compounding Savings Accounts and Investments

\n\nCompound interest isn't just a theoretical concept; it's at play in many of your financial products. Let's look at some common scenarios:

\n\nHigh-Yield Savings Accounts Maximizing Your Cash Growth

\n\nEven in a savings account, compound interest works its magic. While traditional bank savings accounts might offer paltry interest rates, high-yield savings accounts (HYSAs) can provide significantly better returns. These accounts typically compound interest monthly or even daily, which means your money grows faster. They're a great place for your emergency fund or short-term savings goals because they offer liquidity while still providing a decent return.

\n\nRecommended High-Yield Savings Accounts for Compounding:

\n\n- \n

- Ally Bank Online Savings Account: Ally is consistently praised for its competitive interest rates, no monthly fees, and 24/7 customer service. They offer daily compounding, which means your interest starts earning interest almost immediately. As of late 2023/early 2024, their APY (Annual Percentage Yield) has been very attractive, often among the top tier. \n

- Marcus by Goldman Sachs Online Savings Account: Marcus also offers strong APYs, no fees, and a user-friendly online platform. Their interest compounds daily and is paid monthly. They often have promotional rates for new customers. \n

- Discover Bank Online Savings Account: Known for its excellent customer service and competitive rates, Discover Bank's online savings account also compounds interest daily and pays monthly. No monthly fees or minimum balance requirements. \n

- CIT Bank Platinum Savings: This account offers tiered interest rates, meaning higher balances earn higher APYs. Interest is compounded daily and paid monthly. It's a good option if you have a larger sum to save. \n

Usage Scenario: You're building an emergency fund of $10,000. Instead of letting it sit in a checking account earning nothing, putting it in an HYSA like Ally Bank means that $10,000 could grow to $10,300 or more in a year (depending on the APY), simply by letting compound interest work. Over five years, that difference becomes even more substantial.

\n\nCertificates of Deposit (CDs) Locking in Higher Rates

\n\nCDs are another excellent way to leverage compound interest, especially if you have money you don't need for a specific period. You deposit a sum for a fixed term (e.g., 6 months, 1 year, 5 years) and earn a fixed interest rate. The interest on CDs often compounds daily or monthly, and while you can't access the principal without penalty, the guaranteed return and compounding effect make them attractive for specific savings goals.

\n\nRecommended CD Products for Compounding:

\n\n- \n

- Synchrony Bank CDs: Synchrony often offers some of the highest CD rates across various terms. They compound interest daily and credit it monthly. They have a wide range of terms from 3 months to 5 years. \n

- Capital One 360 CDs: Known for their simplicity and no-fee structure, Capital One 360 CDs offer competitive rates and compound interest daily. They are a good choice for those who prefer a well-known brand with a strong online presence. \n

- Barclays Online CDs: Barclays offers competitive rates and a variety of terms. Interest is compounded daily and paid monthly. They are a solid option for those looking for good rates from an established international bank. \n

Usage Scenario: You're saving for a down payment on a house in three years and have $20,000 set aside. Investing this in a 3-year CD with a 4.5% APY (compounded daily) means your $20,000 could grow to over $22,800 by the end of the term, providing a significant boost to your down payment without any active management.

\n\nRetirement Accounts The Long-Term Compounding Powerhouse

\n\nThis is where compound interest truly shines. Retirement accounts like 401(k)s and IRAs are designed for long-term growth, making them perfect vehicles for compounding. The money you contribute, plus any employer match, grows tax-deferred (or tax-free in the case of Roth accounts), allowing compound interest to work its magic uninterrupted for decades.

\n\nRecommended Retirement Account Platforms for Compounding:

\n\n- \n

- Fidelity Investments: A giant in the investment world, Fidelity offers a wide range of investment options (ETFs, mutual funds, stocks) within their 401(k)s and IRAs. Their low-cost index funds are excellent for long-term compounding. \n

- Vanguard: Famous for its low-cost index funds and ETFs, Vanguard is a favorite among long-term investors. Their target-date funds are particularly good for hands-off retirement saving, automatically adjusting asset allocation as you approach retirement. \n

- Charles Schwab: Another top-tier brokerage, Charles Schwab offers a comprehensive suite of investment products and services for retirement accounts. They also have a strong selection of commission-free ETFs. \n

- Betterment / Wealthfront (Robo-Advisors): If you prefer a more automated approach, robo-advisors like Betterment and Wealthfront manage diversified portfolios for you, leveraging ETFs that benefit from compounding. They automatically rebalance and reinvest dividends, maximizing the compounding effect. \n

Usage Scenario: You start contributing $300 a month to a Roth IRA at age 25, earning an average annual return of 7% (compounded annually). By age 65, your initial contributions of $144,000 would have grown to over $700,000, largely due to the power of compounding over 40 years. If you waited until age 35, your total would be significantly less, highlighting the importance of starting early.

\n\nInvestment Accounts Stocks, ETFs, and Mutual Funds

\n\nBeyond dedicated retirement accounts, general investment accounts also benefit immensely from compounding. When you invest in stocks that pay dividends, or mutual funds/ETFs that reinvest their earnings, those reinvested amounts buy more shares, which then earn more dividends or grow in value, creating a powerful compounding loop.

\n\nRecommended Investment Platforms for Compounding:

\n\n- \n

- M1 Finance: M1 Finance is unique for its 'pie' investing approach, allowing you to build a custom portfolio of stocks and ETFs. It automatically reinvests dividends and rebalances your portfolio, making it excellent for hands-off compounding. No management fees for basic accounts. \n

- Robinhood: While known for commission-free stock trading, Robinhood also allows for fractional share investing and dividend reinvestment, making it accessible for smaller investors to benefit from compounding. \n

- Fidelity Go / Schwab Intelligent Portfolios (Robo-Advisors): These are robo-advisor services offered by traditional brokerages. They build and manage diversified portfolios for you, automatically reinvesting dividends and rebalancing, ensuring continuous compounding. Fidelity Go has no advisory fee for balances under $25,000, and Schwab Intelligent Portfolios have no advisory fees at all. \n

Usage Scenario: You invest $5,000 in an S&P 500 index ETF that yields 2% in dividends annually and grows at an average of 8% per year. If you set up dividend reinvestment, those dividends buy more shares. Over 10 years, your initial $5,000 could grow to over $10,000, with a significant portion of that growth coming from the reinvested dividends compounding over time.

\n\nThe Time Factor Why Starting Early Matters

\n\nThe single most important variable in the compound interest equation is time. The longer your money has to grow, the more significant the compounding effect becomes. This is often referred to as the "magic of starting early." Even small, consistent contributions made over a long period can outperform larger, later contributions.

\n\nConsider two individuals: Sarah starts investing $200 a month at age 25 and stops at age 35 (10 years of contributions). John starts investing $200 a month at age 35 and continues until age 65 (30 years of contributions). Assuming a 7% annual return, Sarah, who only contributed for 10 years, will likely have more money at age 65 than John, who contributed for 30 years! This is because Sarah's money had an extra 10 years to compound without interruption. It's a powerful illustration of how time amplifies returns.

\n\nAvoiding Common Pitfalls Maximizing Your Compounding Potential

\n\nWhile compound interest is powerful, there are a few things that can hinder its effectiveness:

\n\nHigh Fees and Expenses Eating Away at Returns

\n\nFees, even seemingly small ones, can significantly erode your returns over time, especially when compounding is at play. A 1% annual fee on an investment that grows at 7% means you're losing a substantial portion of your potential gains. Always look for low-cost investment options, such as index funds and ETFs, and be mindful of account maintenance fees.

\n\nFrequent Withdrawals Interrupting the Growth Cycle

\n\nEvery time you withdraw money from your savings or investment accounts, you're taking away principal that would have otherwise compounded. Try to avoid dipping into your long-term savings unless absolutely necessary. This is why having a separate emergency fund is crucial – it prevents you from derailing your compounding efforts for unexpected expenses.

\n\nLow Interest Rates The Compounding Slowdown

\n\nWhile some interest is better than no interest, very low interest rates (like those often found in traditional checking or basic savings accounts) won't give you much compounding power. Seek out high-yield options for your cash savings and consider diversified investments for long-term growth to get better returns.

\n\nPutting Compounding to Work Your Action Plan

\n\nReady to harness the power of compound interest? Here's your action plan:

\n\n- \n

- Start Early: The sooner you begin saving and investing, the more time your money has to compound. Even small amounts add up significantly over decades. \n

- Be Consistent: Regular contributions, even if modest, are more effective than sporadic large deposits. Automate your savings to make it effortless. \n

- Choose High-Yield Accounts: For your cash savings, opt for high-yield savings accounts or CDs that offer competitive interest rates and frequent compounding. \n

- Invest for the Long Term: For wealth building, utilize retirement accounts (401k, IRA) and brokerage accounts. Invest in diversified, low-cost funds that reinvest dividends. \n

- Minimize Fees: Be vigilant about fees. They are the silent killers of compounding returns. \n

- Avoid Unnecessary Withdrawals: Let your money grow undisturbed. Build an emergency fund to cover unexpected costs so you don't have to tap into your long-term investments. \n

Compound interest isn't a get-rich-quick scheme. It's a slow, steady, and incredibly powerful force that, when understood and utilized correctly, can dramatically accelerate your journey towards financial freedom. So, start today, be patient, and watch your money grow!

" } ] }:max_bytes(150000):strip_icc()/277019-baked-pork-chops-with-cream-of-mushroom-soup-DDMFS-beauty-4x3-BG-7505-5762b731cf30447d9cbbbbbf387beafa.jpg)