How to Create a Retirement Income Strategy

Practical advice on how to develop a robust retirement income strategy to ensure a steady cash flow.

Practical advice on how to develop a robust retirement income strategy to ensure a steady cash flow.

How to Create a Retirement Income Strategy

Understanding Your Retirement Income Needs

Alright, so you've been saving for retirement, which is awesome! But saving is just one piece of the puzzle. The real magic happens when you figure out how to turn those savings into a steady stream of income that lasts throughout your golden years. This isn't just about having a big nest egg; it's about making sure that nest egg works for you, providing enough cash to cover your living expenses, enjoy your hobbies, and maybe even spoil the grandkids a little. The first step in creating a robust retirement income strategy is to truly understand your needs. This means getting a clear picture of what your expenses will look like in retirement. Will your mortgage be paid off? What about healthcare costs, which tend to rise as we age? Are you planning on traveling the world, or do you envision a more relaxed life at home? These are crucial questions because they directly impact how much income you'll need. Many people underestimate their retirement expenses, especially when it comes to healthcare and leisure activities. It's not just about replacing your pre-retirement income; it's about funding the lifestyle you desire. Think about your current spending habits and then project them into retirement, adjusting for changes like no more commuting costs or work-related expenses, but potentially higher medical bills or travel budgets. Don't forget about inflation either; what costs $100 today will cost more in 20 or 30 years. A good rule of thumb is to aim for 70-80% of your pre-retirement income, but this can vary wildly based on individual circumstances. Some financial planners even suggest a 'go-go, slow-go, no-go' approach to retirement spending, where expenses might be higher in the early, active years, then moderate, and finally decrease in later, less active years. This dynamic approach can help you tailor your income strategy to different phases of retirement. It's also important to consider any one-time large expenses you might have, like home renovations or helping out family members. These need to be factored into your overall income plan. Getting a realistic handle on your future expenses is the bedrock upon which your entire retirement income strategy will be built. Without this clarity, you're essentially shooting in the dark, and that's not a game you want to play with your financial future.

Key Sources of Retirement Income

Once you've got a handle on your expenses, it's time to look at where that income is actually going to come from. Most people don't rely on just one source; a diversified approach is usually the most resilient. Let's break down the common pillars of retirement income. First up, and often the most foundational, is Social Security. For many, this provides a significant portion of their retirement income. The big question here is when to claim it. You can start as early as age 62, but your benefits will be permanently reduced. Waiting until your Full Retirement Age (FRA), which is typically between 66 and 67 depending on your birth year, gets you 100% of your earned benefits. And if you can hold out until age 70, you'll get an even larger benefit, increasing by about 8% for each year you delay past your FRA. This decision can have a massive impact on your lifetime income, so it's worth careful consideration, often in consultation with a financial advisor. Your health, other income sources, and life expectancy all play a role in this choice. Next, we have your personal savings and investments. This is where all those years of contributing to your 401(k), IRA, Roth IRA, and taxable brokerage accounts come into play. This is often the largest and most flexible source of retirement income. You'll need a strategy for drawing down these assets, often referred to as the 'withdrawal strategy.' The 4% rule is a popular guideline, suggesting you can withdraw 4% of your initial portfolio value in the first year of retirement, and then adjust that amount for inflation in subsequent years. While a good starting point, it's not a hard and fast rule and might need to be adjusted based on market conditions and your specific situation. Some advisors advocate for a more dynamic withdrawal strategy, adjusting withdrawals based on portfolio performance. Then there are pensions, if you're lucky enough to have one. These are becoming rarer, but if you have a defined benefit plan from a former employer, it can provide a guaranteed income stream for life. Understanding your pension options, such as lump sum vs. annuity payments, is crucial. Finally, don't forget about other potential income sources. This could include rental income from properties, part-time work or consulting in retirement, or even annuities purchased from insurance companies. Annuities can provide a guaranteed income stream for life, similar to a pension, and can be a good option for those who want to reduce market risk in their income plan. However, they come with their own complexities and fees, so thorough research is essential. By combining these various sources, you can create a diversified and robust income stream that can weather different economic conditions and provide peace of mind throughout your retirement.

Developing a Withdrawal Strategy: The 4% Rule and Beyond

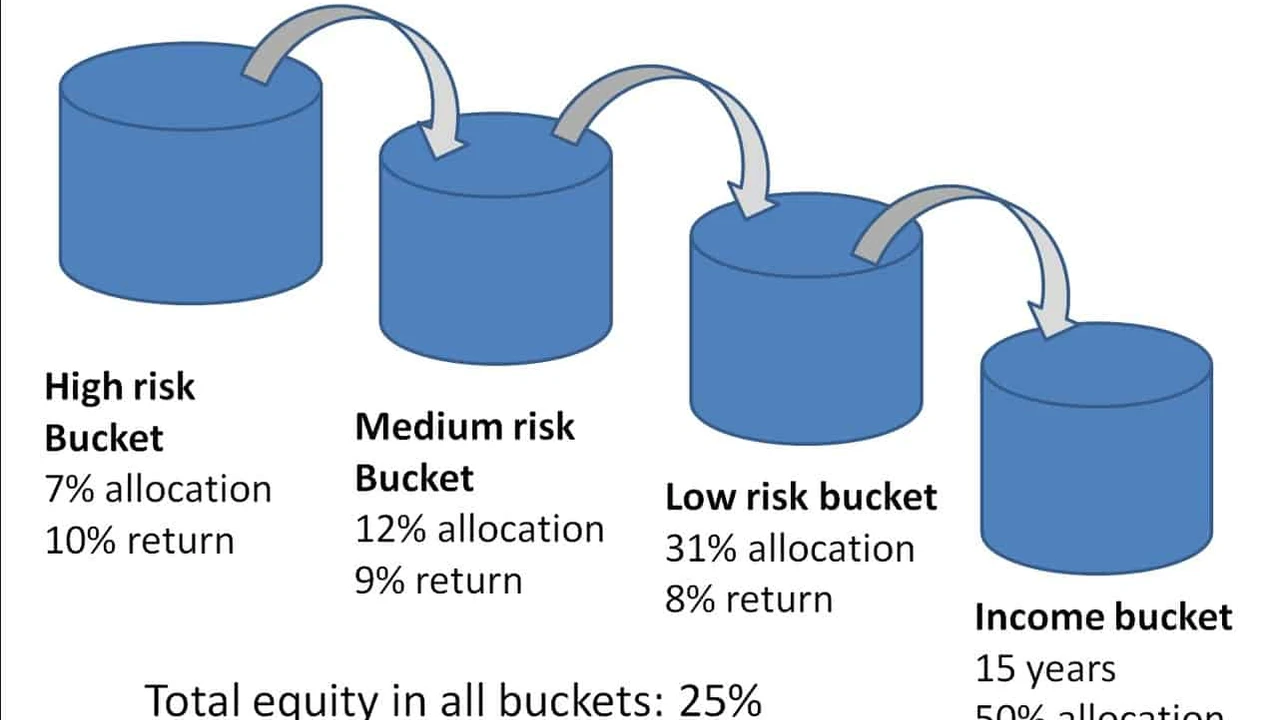

Okay, so you've got your nest egg, but how do you actually take money out of it without running out? This is where your withdrawal strategy comes in, and it's one of the most critical components of your retirement income plan. The most famous guideline is the '4% Rule.' This rule suggests that you can safely withdraw 4% of your initial retirement portfolio balance in your first year of retirement, and then adjust that amount for inflation in subsequent years, with a high probability that your money will last for 30 years or more. For example, if you retire with $1,000,000, you'd withdraw $40,000 in your first year. If inflation is 3% the next year, you'd withdraw $41,200. This rule was popularized by financial planner William Bengen in the mid-1990s, based on historical market data. It's a great starting point for planning, offering a simple benchmark. However, it's not a one-size-fits-all solution. Market conditions, your specific asset allocation, and your actual retirement horizon can all influence its effectiveness. For instance, if you retire during a bear market, sticking rigidly to the 4% rule might deplete your portfolio faster than intended. This is known as 'sequence of returns risk.' To mitigate this, some financial advisors advocate for more flexible or dynamic withdrawal strategies. One such approach is the 'Guardrails Strategy.' With this method, you set an initial withdrawal rate (e.g., 4%), but then adjust it up or down based on your portfolio's performance. If your portfolio performs exceptionally well, you might allow for a slightly higher withdrawal. If it struggles, you might reduce your withdrawal for a year or two to preserve capital. This flexibility can significantly increase the longevity of your portfolio. Another strategy is the 'Bucket Strategy.' This involves dividing your retirement assets into different 'buckets' based on when you'll need the money. For example, one bucket might hold cash for immediate expenses (1-2 years), another might hold conservative investments for short-term needs (3-5 years), and a third might hold growth-oriented investments for long-term needs (5+ years). You draw from the cash bucket first, allowing the other buckets to grow. When the cash bucket gets low, you replenish it from the conservative bucket, and so on. This can provide psychological comfort and a clearer roadmap for withdrawals. There's also the 'Time-Segmentation Strategy,' which is similar to the bucket strategy but often more explicitly tied to specific years of expenses. For example, you might have enough cash for the first 5 years, bonds for the next 10, and stocks for the years beyond that. The key takeaway here is that while the 4% rule is a good starting point, exploring more dynamic or segmented withdrawal strategies can provide greater flexibility and resilience, especially in uncertain market environments. It's about finding a strategy that aligns with your risk tolerance, your financial goals, and your comfort level with adjusting your spending in retirement. Don't be afraid to consult with a financial professional to tailor a withdrawal strategy that's perfect for you.

Product Spotlight: Annuities for Guaranteed Income

While your investment portfolio is a fantastic source of flexible income, some people crave the certainty of a guaranteed paycheck in retirement, much like a traditional pension. This is where annuities come into play. An annuity is essentially a contract with an insurance company where you pay a lump sum or a series of payments, and in return, the company promises to pay you a regular income stream, either for a set period or for the rest of your life. They can be a powerful tool for mitigating longevity risk – the risk of outliving your savings. Let's look at a few types and some specific product examples, keeping in mind that annuity products are complex and vary widely by provider and state regulations. Always consult with a licensed financial advisor before making any annuity purchase.

Immediate Annuities (Single Premium Immediate Annuity - SPIA)

These are the simplest form. You pay a single lump sum, and income payments start almost immediately (within a year). They're great for converting a portion of your savings into a guaranteed income stream right at the start of retirement. The income amount is fixed and guaranteed for life, regardless of market performance. This provides incredible peace of mind for covering essential expenses.

- Product Example: Many major insurance companies offer SPIAs. For instance, New York Life's Guaranteed Future Income Annuity or MassMutual's Immediate Income Annuity.

- Use Case: Ideal for retirees who want to cover their basic living expenses with a guaranteed income stream, ensuring they won't run out of money for necessities. It's often used to supplement Social Security.

- Comparison: Simpler and often less expensive than other annuity types. The trade-off is less flexibility once payments begin. You're essentially trading a lump sum for a guaranteed income stream.

- Pricing/Payout: Payouts depend on your age, gender, the amount invested, and current interest rates. A 65-year-old male investing $100,000 might receive around $500-$600 per month for life, but this is a rough estimate and varies significantly.

Deferred Annuities (Fixed, Variable, Indexed)

With deferred annuities, your money grows over time before you start receiving payments. You can contribute a lump sum or make periodic payments. The growth phase is called the accumulation phase, and the income phase is called the annuitization phase. They come in different flavors:

Fixed Deferred Annuities

These offer a guaranteed interest rate for a set period, similar to a CD. Your principal is protected, and growth is predictable.

- Product Example: Athene Ascent Fixed Annuity or Pacific Life Pacific Index Foundation (though this one has indexed features, some fixed options exist).

- Use Case: For those who want tax-deferred growth and principal protection, but aren't ready to start receiving income yet. Good for conservative investors.

- Comparison: Less growth potential than variable or indexed annuities, but no market risk. Simpler than indexed annuities.

- Pricing/Rates: Interest rates vary but might be in the 2-4% range, often guaranteed for 3-10 years. Surrender charges apply if you withdraw money early.

Variable Deferred Annuities

Your money is invested in sub-accounts, similar to mutual funds. The value of your annuity and your future income payments can fluctuate with market performance. These offer growth potential but also market risk.

- Product Example: Jackson National Perspective II Variable Annuity or Prudential Defined Income Variable Annuity.

- Use Case: For investors comfortable with market risk who want tax-deferred growth and potentially higher returns. Often includes optional riders for guaranteed income or death benefits.

- Comparison: Highest growth potential among annuities, but also highest risk. More complex and typically higher fees than fixed annuities.

- Pricing/Fees: Can have multiple layers of fees: mortality & expense (M&E) fees (around 1.25% annually), administrative fees, sub-account fees (0.5-2% annually), and rider fees (0.5-1.5% annually). Total fees can easily exceed 3% per year.

Indexed Deferred Annuities (Fixed Indexed Annuities - FIAs)

These offer a blend of fixed and variable. Your growth is linked to a market index (like the S&P 500) but with downside protection. You participate in some of the market's gains, up to a cap or participation rate, but you don't lose money if the market declines.

- Product Example: Allianz 222 Annuity or American Equity Bonus Gold.

- Use Case: For those who want market-linked growth potential without the risk of losing principal. A good middle ground between fixed and variable.

- Comparison: More complex than fixed annuities, less growth potential than variable annuities (due to caps/participation rates), but offers principal protection.

- Pricing/Fees: Generally lower annual fees than variable annuities (often 0-1% for the base contract), but growth is limited by caps (e.g., 8% annual cap) or participation rates (e.g., 70% of index gains). Surrender charges are common.

Longevity Annuities (Qualified Longevity Annuity Contract - QLAC)

A specific type of deferred annuity designed to protect against outliving your money in very old age. You invest a lump sum, but payments don't start until much later, often age 80 or 85. This allows for smaller initial premiums for a large future payout.

- Product Example: Many providers offer QLACs, including Fidelity Personal Retirement Annuity QLAC or TIAA-CREF QLAC.

- Use Case: For individuals concerned about running out of money in their very late retirement years. It's a form of insurance against extreme longevity.

- Comparison: Payments start much later than SPIAs, but the initial investment is smaller for a given future income. Can be purchased with qualified (pre-tax) retirement funds.

- Pricing/Payout: Payouts are highly dependent on the deferral period. A $100,000 investment at age 65 might provide $2,000-$3,000 per month starting at age 85, but again, this is highly variable.

When considering annuities, it's crucial to understand the surrender charges (penalties for early withdrawal), riders (optional add-ons like guaranteed income benefits or death benefits, which add to fees), and the financial strength of the insurance company. Annuities are long-term contracts, and they're not for everyone. They can be illiquid and complex. However, for those seeking a guaranteed income floor in retirement, they can be a valuable piece of the puzzle, especially when used strategically as part of a broader, diversified income plan.

Optimizing Tax Efficiency in Retirement Withdrawals

You've worked hard to save your money, and the last thing you want is for taxes to eat away at your retirement income. A smart retirement income strategy isn't just about how much you withdraw, but also about how you withdraw it to minimize your tax burden. This often involves a careful sequencing of withdrawals from different types of accounts. Generally, you'll have three main types of accounts: tax-deferred (like traditional 401(k)s and IRAs), tax-free (like Roth 401(k)s and Roth IRAs), and taxable (like brokerage accounts). Each has different tax implications in retirement.

The General Withdrawal Order

A common strategy for tax-efficient withdrawals is to follow this order:

- Taxable Accounts First: Many financial planners suggest drawing from your taxable brokerage accounts first. The gains in these accounts are subject to capital gains taxes, which are often lower than ordinary income tax rates, especially if you've held the investments for over a year (long-term capital gains). By drawing from these first, you allow your tax-deferred and tax-free accounts to continue growing. This also gives you flexibility, as you can choose which specific investments to sell to manage your capital gains.

- Tax-Deferred Accounts Next: Once your taxable accounts are depleted or you want to preserve them, you'd move to your tax-deferred accounts (traditional 401(k), traditional IRA). Withdrawals from these accounts are taxed as ordinary income. The goal here is to manage your withdrawals to stay within lower tax brackets. This is where strategic planning comes in. You might take just enough to cover your expenses, or even do 'Roth conversions' in years where your income is low (e.g., early retirement before Social Security or RMDs kick in) to convert pre-tax money to tax-free money in a Roth account.

- Tax-Free Accounts Last: Your Roth accounts (Roth IRA, Roth 401(k)) are generally the last money you touch. Why? Because qualified withdrawals from these accounts are completely tax-free. By letting them grow for as long as possible, you maximize their tax-free compounding. This also provides a fantastic source of emergency funds or a way to pay for large, unexpected expenses without incurring additional taxes. Plus, Roth IRAs don't have Required Minimum Distributions (RMDs) for the original owner, meaning you can leave the money to your heirs tax-free.

Other Tax Optimization Strategies

- Required Minimum Distributions (RMDs): Remember that once you reach age 73 (or 75 for those born in 1960 or later), you'll be required to start taking RMDs from your traditional IRAs and 401(k)s. These withdrawals are taxable income, and failing to take them results in a hefty penalty. Factor these into your income plan.

- Roth Conversions: As mentioned, converting money from a traditional IRA to a Roth IRA can be a powerful tax strategy, especially in years where you expect to be in a lower tax bracket. You pay taxes on the converted amount now, but all future growth and withdrawals are tax-free. This can be particularly useful in the 'retirement gap' years between early retirement and when Social Security or RMDs begin.

- Tax Loss Harvesting: In your taxable accounts, if you have investments that have lost value, you can sell them to realize a loss. This loss can then be used to offset capital gains and even a limited amount of ordinary income ($3,000 per year). This can reduce your overall tax bill.

- Qualified Charitable Distributions (QCDs): If you're charitably inclined and over age 70.5, you can make a QCD directly from your IRA to a qualified charity. This amount counts towards your RMD but isn't included in your taxable income, which can be a significant tax benefit.

- Healthcare Expenses and HSAs: If you have a Health Savings Account (HSA), it's a triple-tax-advantaged account (tax-deductible contributions, tax-free growth, tax-free withdrawals for qualified medical expenses). Many people use HSAs as a supplemental retirement savings vehicle, especially for healthcare costs. If you can pay for medical expenses out-of-pocket during your working years, you can let your HSA grow and use it tax-free in retirement for medical costs, or even for general living expenses after age 65 (though these withdrawals would be taxed as ordinary income).

Navigating the tax landscape in retirement can be complex, and tax laws change. It's highly recommended to work with a financial advisor and a tax professional to create a personalized tax-efficient withdrawal strategy that aligns with your specific financial situation and goals. The goal is to keep more of your hard-earned money in your pocket and less in Uncle Sam's.

Monitoring and Adjusting Your Plan

Creating a retirement income strategy isn't a one-and-done deal. Life happens, markets fluctuate, and your needs and goals might change over time. That's why regular monitoring and adjustment are absolutely crucial for the long-term success of your plan. Think of it like navigating a ship; you set a course, but you constantly check your position and adjust for winds, currents, and unexpected storms. The same goes for your retirement income. You should aim to review your plan at least once a year, or more frequently if there are significant life events or market shifts.

What to Monitor

- Your Spending: Are your actual expenses aligning with your projections? Are you spending more or less than anticipated? Unexpected large expenses (like home repairs or medical bills) can throw off your plan. Conversely, if you're spending less, you might have more flexibility.

- Portfolio Performance: How are your investments performing? Are they generating the returns you expected? A prolonged bear market could necessitate a temporary reduction in withdrawals, while a strong bull market might allow for a slight increase or provide a buffer.

- Inflation: Inflation erodes purchasing power. Are your income sources keeping pace with rising costs? If inflation is higher than anticipated, your fixed income streams might not stretch as far, requiring adjustments to your withdrawal rate or a re-evaluation of your income sources.

- Tax Laws: Tax laws can change, impacting your withdrawal strategy. Stay informed about any new legislation that could affect your retirement income.

- Health and Longevity: Your health status can impact your expenses (especially healthcare) and your expected lifespan. If your health declines, you might need to adjust your spending or consider long-term care options. If you're living longer than expected, you'll need your money to last longer.

- Social Security and Pension Changes: While generally stable, there can be adjustments to Social Security benefits or pension rules. Stay updated on any changes that might affect your guaranteed income.

When to Adjust

Adjustments aren't necessarily about cutting back; they can also be about optimizing. Here are some scenarios that might trigger an adjustment:

- Significant Market Downturn: If your portfolio takes a big hit early in retirement, consider temporarily reducing your withdrawals to avoid locking in losses. This is where the 'guardrails' strategy comes in handy.

- Unexpected Windfall: Did you receive an inheritance or sell a property for more than expected? This could provide an opportunity to replenish your savings, increase your income, or make a large purchase.

- Major Life Events: Marriage, divorce, the death of a spouse, or a new grandchild can all impact your financial needs and goals.

- Healthcare Needs: A new diagnosis or the need for long-term care can significantly increase expenses, requiring a re-evaluation of your income sources.

- Changes in Lifestyle: Deciding to travel more, take up an expensive hobby, or move to a different location will all have financial implications.

How to Adjust

Adjustments can take many forms:

- Modifying Withdrawal Rates: This is the most direct way to respond to changes in your portfolio or expenses.

- Rebalancing Your Portfolio: Ensure your asset allocation still aligns with your risk tolerance and time horizon. You might need to shift more towards income-generating assets or adjust your equity exposure.

- Exploring Additional Income Sources: Could a part-time job, consulting, or a reverse mortgage be an option if you're facing a shortfall?

- Revisiting Annuity Options: If you're concerned about longevity risk, purchasing a deferred annuity later in retirement could provide a guaranteed income floor.

- Optimizing Tax Strategies: Re-evaluate your Roth conversion strategy or other tax-efficient withdrawal methods based on current tax laws and your income levels.

Regular reviews, ideally with a qualified financial advisor, will help you stay on track and make informed decisions. Your retirement income strategy is a living document, not a static plan. By being proactive and flexible, you can ensure your money lasts as long as you do, allowing you to enjoy your retirement years with confidence and peace of mind.

:max_bytes(150000):strip_icc()/277019-baked-pork-chops-with-cream-of-mushroom-soup-DDMFS-beauty-4x3-BG-7505-5762b731cf30447d9cbbbbbf387beafa.jpg)